Favorite Adjusting Entry For Salaries Payable Basic Accounting Balance Sheet

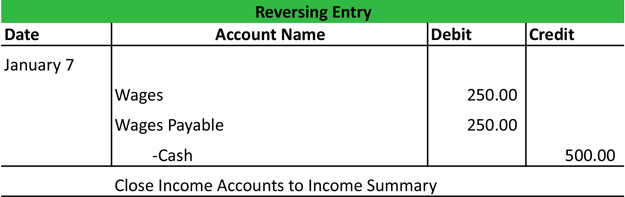

Reversing Entries Accounting Example Requirements Explained

Salary expense for the period was 1100 and 1400 was paid to employees in cash. Examples include utility bills salaries and taxes which are usually charged in a later period after they have been incurred. Unless a company pays salaries on the last day of the accounting period for a pay period ending on that date it must make an adjusting entry to record any salaries incurred but not yet paid. Adjusting Entry - Wage Expense. Example- On 1st March Company A Ltd paid 4 months prepaid salary amounting to 40000 100004 to the employees of the company. The 1500 balance in Wages Payable is the true amount not yet paid to employees for their work through December 31. Salary expense for the period was 1100 and 1400 was paid to employees in cash. Any hours worked in. Salary expense for the period was 1100 and 1400 was paid to employees in cash. Adjusting Entry - Salaries Payable.

If Moon company makes adjusting entries at the end of each month it will record the following adjusting entry on January 31.

Adjusting Entry - Salaries Payable Practice Problem - Acg 2021 Florida International University. Journal Entries for Salaries Payable There are two steps to think about when we think about Salaries Payable. Adjusting entry on January 31. The total salary payable for the month of January is 8500. Adjusting Entry - Wage Expense. Adjusting Entry - Salaries Payable Practice Problem - Acct 229 Texas AM.

Adjusting entry on January 31. Adjusting Entry - Wage Expense. It is further shown under the head current asset in the balance sheet. Salaries payable at the end of the period was 500. Salary expense for the period was 1100 and 1400 was paid to employees in cash. Any hours worked in. Examples include utility bills salaries and taxes which are usually charged in a later period after they have been incurred. The 1500 balance in Wages Payable is the true amount not yet paid to employees for their work through December 31. The 13420 of Wages Expense is the total of the wages used by the company through December 31. If you keep the books yourself you can be more informative and label it Adjusting Entry for Accrued Wages or something similar to help you remember more clearly what youve done.

Adjusting Entry - Salaries Payable. The Wages Payable amount will be carried forward to the next accounting year. Salaries payable at the end of the period was 500. Hence prepaid salary or salary paid in advance is treated as adjustment entry. Published on April 12 2015Downloads for YT. What should the adjusting entry. This video is about the AJE required when payday is not the same as the end of the period. Examples include utility bills salaries and taxes which are usually charged in a later period after they have been incurred. The total salary payable for the month of January is 8500. Debit salaries expense and credit salaries payable to record the accrued salaries.

Published on April 12 2015Downloads for YT. Unless a company pays salaries on the last day of the accounting period for a pay period ending on that date it must make an adjusting entry to record any salaries incurred but not yet paid. Adjusting Entry - Salaries Payable in Chapter 3 Problem 12 of 20 Moderate. The 1500 balance in Wages Payable is the true amount not yet paid to employees for their work through December 31. Adjusting Entry - Salaries Payable Practice Problem - Acct 229 Texas AM. Payroll expense is the operating expense that should record in the month of occurrence. What was salaries payable at the beginning of the period. However the salary for last month is not yet paid so they prepare adjusting entry for this transaction. Adjusting entry on January 31. Salary expense for the period was 1100 and 1400 was paid to employees in cash.

Adjusting Entry - Salaries Payable. The recording of the payment of employee salaries usually involves a debit to an expense account and a credit to Cash. If you keep the books yourself you can be more informative and label it Adjusting Entry for Accrued Wages or something similar to help you remember more clearly what youve done. Adjusting Entry - Salaries Payable. Adjusting Entry - Salaries Payable in Chapter 3 Problem 12 of 20 Moderate. The Moon company pays salary to its employees on fifth day of every month. Salary expense for the period was 1100 and 1400 was paid to employees in cash. It is further shown under the head current asset in the balance sheet. What should the adjusting entry. Adjusting Entry - Salaries Payable.

Adjusting Entry - Salaries Payable. The first step being the Accrual of Salaries on the company books for all the time that the employees have worked. When the cash is paid an adjusting entry is made to remove the account payable that was recorded together with the accrued expense previously. It is further shown under the head current asset in the balance sheet. The total salary payable for the month of January is 8500. Salary expense for the period was 1100 and 1400 was paid to employees in cash. Adjusting Entry - Salaries Payable. Published on April 12 2015Downloads for YT. Unless a company pays salaries on the last day of the accounting period for a pay period ending on that date it must make an adjusting entry to record any salaries incurred but not yet paid. The Wages Payable amount will be carried forward to the next accounting year.