Cool Balance Sheet Approach Allowance For Doubtful Accounts Edgar Financial Data

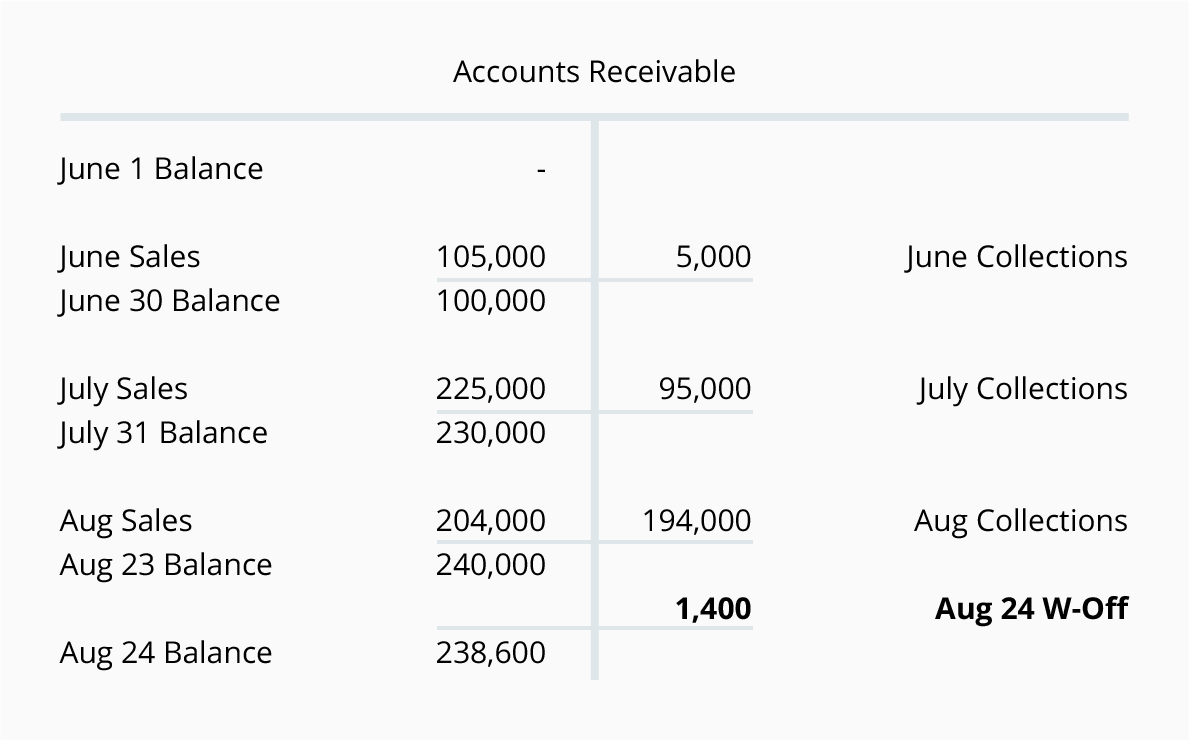

Writing Off An Account Under The Allowance Method Accountingcoach

This means that in order to present an accurate assessment of AR we need to determine how many AR are not receivable in full. Effective market rate of interest for these bonds is 8. Definition of Allowance for Doubtful Accounts. This amount is referred to as the net realizable value of the accounts receivable the amount that is likely to be turned into cash. The allowance for doubtful accounts is a reduction of the total amount of accounts receivable appearing on a companys balance sheet and is listed as a deduction immediately below the accounts receivable line item. The use of this allowance account will result in a more realistic picture of the amount of the accounts receivable that will be turning to cash since some customers may not pay the full amount owed to the company. The balance in allowance for doubtful accounts is 650 before making adjusting entry for uncollectible accounts expense. The Balance-Sheet Approach to Estimate Bad Debt. Calculate allowance for doubtful accounts using sales method or income statement approach. Add the current positive or negative account balance to your allowance estimate so the journal entry makes the final account balance the same as your estimate.

The allowance for doubtful accounts adjusting entry would be 20000.

Allowance for doubtful is the contra asset account with accounts receivable which present in the balance sheet. This amount is referred to as the net realizable value of the accounts receivable the amount that is likely to be turned into cash. Definition of Allowance for Doubtful Accounts. The allowance of doubtful accounts had a credit balance of 1600. An allowance for doubtful accountsalso known as an ADA an allowance for bad debt or a bad debt allowanceis a contra asset account which is an account that either has a balance of zero or a credit balance and it is associated with your accounts receivable. Martin MFG company uses balance sheet approach to calculate allowance for doubtful accounts and bad debt expense.

Definition of Allowance for Doubtful Accounts. The allowance for doubtful accounts adjusting entry would be 20000. Most people may confuse this account as the liability but it is not even it is a negative asset account. Allowance for Doubtful Accounts. Martin MFG company issued 10 stated rate bonds in 2020. For example if the Allowance for Doubtful Accounts presently has a credit balance of 2000 and you believe there is a total of 2900 in Accounts Receivable that will not be collected you. The balance sheet approach estimates the allowance for doubtful accounts based on the accounts receivable balance at the end of each period. Allowance for doubtful is the contra asset account with accounts receivable which present in the balance sheet. Add the current positive or negative account balance to your allowance estimate so the journal entry makes the final account balance the same as your estimate. An allowance for doubtful accounts is a contra entry which is passed in the accounting field to net off the total amount of receivables which are present on the balance sheet to show only the specific amounts which are to paid as expected and thus allowance of doubtful accounts is just estimation of the amount of receivables which the business expects cannot.

Allowance for doubtful accounts on the Balance Sheet. This amount is referred to as the net realizable value of the accounts receivable the amount that is likely to be turned into cash. The balance sheet approach estimates the allowance for doubtful accounts based on the accounts receivable balance at the end of each period. With the account reporting a credit balance of 50000 the balance sheet will report a net amount of 9950000 for accounts receivable. The allowance for doubtful accounts is a reduction of the total amount of accounts receivable appearing on a companys balance sheet and is listed as a deduction immediately below the accounts receivable line item. Most people may confuse this account as the liability but it is not even it is a negative asset account. The Balance-Sheet Approach to Estimate Bad Debt. Thats because the balance sheet-approach calculates what the allowance for doubtful accounts should be not necessarily bad debt expense itself. This deduction is classified as a contra asset account. For example if the Allowance for Doubtful Accounts presently has a credit balance of 2000 and you believe there is a total of 2900 in Accounts Receivable that will not be collected you.

Thats because the balance sheet-approach calculates what the allowance for doubtful accounts should be not necessarily bad debt expense itself. The allowance for doubtful accounts adjusting entry would be 20000. At the end of the year 2016 the allowance for doubtful accounts account shows a credit balance of 2000. The Allowance for Doubtful Accounts is a balance sheet contra asset account that reduces the reported amount of accounts receivable. Martin MFG company issued 10 stated rate bonds in 2020. For example if the Allowance for Doubtful Accounts presently has a credit balance of 2000 and you believe there is a total of 2900 in Accounts Receivable that will not be collected you. With the account reporting a credit balance of 50000 the balance sheet will report a net amount of 9950000 for accounts receivable. The Balance-Sheet Approach to Estimate Bad Debt. Increase in the allowance for doubtful accounts contra-asset. Compute the total amount of estimated uncollectibles the required balance in the allowance for doubtful accounts account on the basis of above information.

The balance in allowance for doubtful accounts is 650 before making adjusting entry for uncollectible accounts expense. Most people may confuse this account as the liability but it is not even it is a negative asset account. The allowance for doubtful accounts is a reduction of the total amount of accounts receivable appearing on a companys balance sheet and is listed as a deduction immediately below the accounts receivable line item. This means that in order to present an accurate assessment of AR we need to determine how many AR are not receivable in full. Martin MFG company issued 10 stated rate bonds in 2020. The Allowance for Doubtful Accounts is a balance sheet contra asset account that reduces the reported amount of accounts receivable. Effective market rate of interest for these bonds is 8. With the account reporting a credit balance of 50000 the balance sheet will report a net amount of 9950000 for accounts receivable. The use of this allowance account will result in a more realistic picture of the amount of the accounts receivable that will be turning to cash since some customers may not pay the full amount owed to the company. Martin MFG company uses balance sheet approach to calculate allowance for doubtful accounts and bad debt expense.

A useful tool in estimating the allowance would be the accounts receivable aging report which states how far past due specific customers balances are that make up accounts receivable. Effective market rate of interest for these bonds is 8. Allowance for Doubtful Accounts. Calculate allowance for doubtful accounts using sales method or income statement approach. At the end of the year 2016 the allowance for doubtful accounts account shows a credit balance of 2000. Martin MFG company issued 10 stated rate bonds in 2020. The allowance for doubtful accounts is a contra asset account and is subtracted from Accounts Receivable to determine the Net Realizable Value of the Accounts Receivable account on the balance sheet. The balance in allowance for doubtful accounts is 650 before making adjusting entry for uncollectible accounts expense. Current policy is to reserve 20 gross accounts receivable as an allowance for uncollectible accounts. An allowance for doubtful accountsalso known as an ADA an allowance for bad debt or a bad debt allowanceis a contra asset account which is an account that either has a balance of zero or a credit balance and it is associated with your accounts receivable.