Recommendation Classification Of Owners Equity Equation For Assets Liabilities And

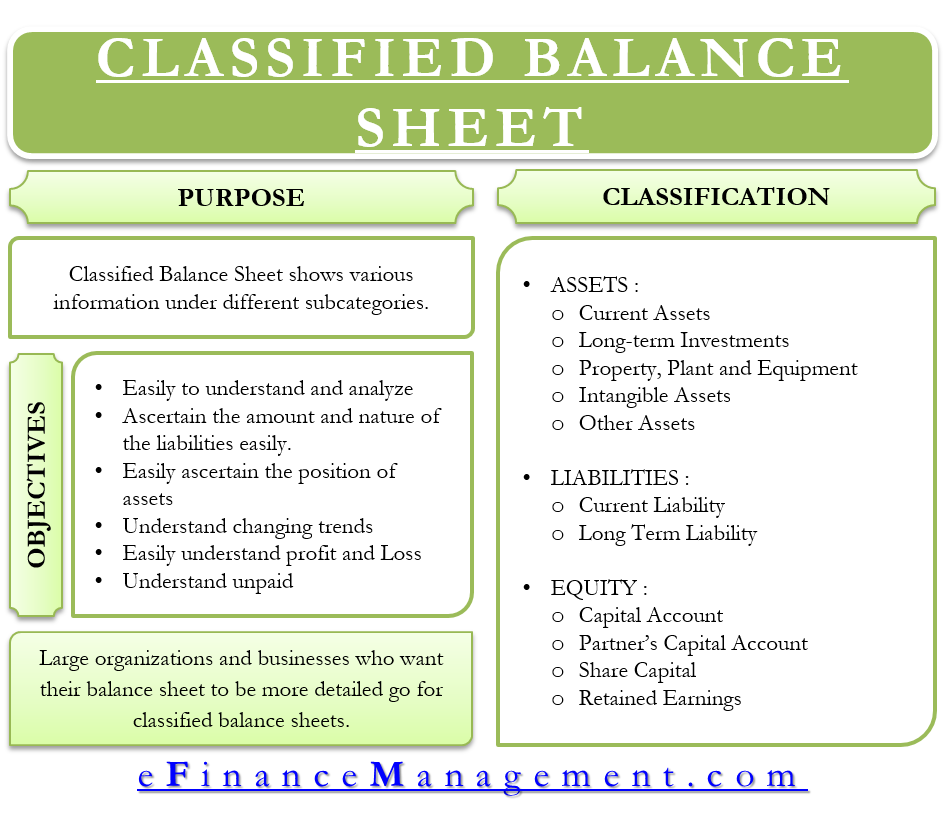

Classified Balance Sheet Meaning Importance Format And More

Capital structures can be complex containing a number of features and performance characteristics. Learning ObjectivesAfter going through this chapter you should be able to. Define explain the balance sheet assets liabilities and owners equity. The owners equity is simply the owners share of the assets of a business. Owners equity is most common for a sole proprietor or business partner. For a small business owner equity is the net worth of your business. The equity accounts are noted below. Pursuant to this section a person deemed a beneficial owner of more than ten percent of any class of equity securities registered under section 12 of the Act would file a Form 3 249103 but the securities holdings disclosed on Form 3 and changes in beneficial ownership reported on subsequent Forms 4 249104 or 5 249105 would be determined by the definition of beneficial owner in paragraph a. A classic reference is Jensen and Meckling 1976 who discussed the nature of agency costs associated with outside claims on the firm - both debt and equity. When you take all of your assets and subtract all of your liabilities you get equity.

The division of owners equity by its sources legal components restric tions classes of stock and utilization are the classifi cation principles that were examined in this study.

Many instruments classified as a financial liability under IFRS could be classified as equity or temporary equity under US GAAP. Define explain the balance sheet assets liabilities and owners equity. People outside the business who you owe money to debts known in accounting as liabilities The owner himself owners equity. Each one is used to store different information about the interests of owners in a business. The owners equity is simply the owners share of the assets of a business. Owners Equity is defined as the proportion of the total value of a companys assets that can be claimed by its owners sole proprietorship or partnership and by.

Pursuant to this section a person deemed a beneficial owner of more than ten percent of any class of equity securities registered under section 12 of the Act would file a Form 3 249103 but the securities holdings disclosed on Form 3 and changes in beneficial ownership reported on subsequent Forms 4 249104 or 5 249105 would be determined by the definition of beneficial owner in paragraph a. There are several types of accounts used to record shareholders equity. For a sole proprietorship or partnership equity is usually called owners equity on the balance sheet. Learning ObjectivesAfter going through this chapter you should be able to. Define understand the use of the accounting equation in analyzing transactions. The types of equity accounts differ depending on whether a business is organized as a corporation or a partnership. When you take all of your assets and subtract all of your liabilities you get equity. List the major subdivisions of the stockholders equity sec- tion of a corporate balance sheet and describe briefly the nature of the amounts that will appear in each section. Equity shares are classified on the basis of different factors. The owners equity is simply the owners share of the assets of a business.

The division of owners equity by its sources legal components restric tions classes of stock and utilization are the classifi cation principles that were examined in this study. The types of equity accounts differ depending on whether a business is organized as a corporation or a partnership. And certain instruments that are equity under IFRS could be classified outside equity under US GAAP. The owners equity is simply the owners share of the assets of a business. For a small business owner equity is the net worth of your business. You can calculate owners equity by subtracting your liabilities from your assets. Recognition and Measurement thereby avoiding the complicated ongoing measurement requirements of. Learning ObjectivesAfter going through this chapter you should be able to. The equity accounts are noted below. Equity classification avoids the negative impact that liability classification has on reported earnings and gearing ratios.

In a corporation equity is shareholders equity. It also results in the instrument falling outside the scope of IAS 39 Financial Instruments. Owners equity is most common for a sole proprietor or business partner. People outside the business who you owe money to debts known in accounting as liabilities The owner himself owners equity. Many instruments classified as a financial liability under IFRS could be classified as equity or temporary equity under US GAAP. Ch 3 accounting equation classification. You see assets can only belong to two types of people. For a small business owner equity is the net worth of your business. The types of equity accounts differ depending on whether a business is organized as a corporation or a partnership. When you take all of your assets and subtract all of your liabilities you get equity.

Capital structures can be complex containing a number of features and performance characteristics. Principles that could be used in the classification of owners equity and to evaluate their appropriateness and usefulness for financial reporting. The types of equity accounts differ depending on whether a business is organized as a corporation or a partnership. ACC 106Chapter 3 Accounting Equation and Classification. The owners equity is simply the owners share of the assets of a business. Owners equity is most common for a sole proprietor or business partner. There are several types of accounts used to record shareholders equity. It also results in the instrument falling outside the scope of IAS 39 Financial Instruments. In a corporation equity is shareholders equity. Different kinds of equity share capital are authorized issued subscribed paid up rights bonus sweat equity etc.

List the major subdivisions of the stockholders equity sec- tion of a corporate balance sheet and describe briefly the nature of the amounts that will appear in each section. Define explain the balance sheet assets liabilities and owners equity. Many instruments classified as a financial liability under IFRS could be classified as equity or temporary equity under US GAAP. The types of equity accounts differ depending on whether a business is organized as a corporation or a partnership. Pursuant to this section a person deemed a beneficial owner of more than ten percent of any class of equity securities registered under section 12 of the Act would file a Form 3 249103 but the securities holdings disclosed on Form 3 and changes in beneficial ownership reported on subsequent Forms 4 249104 or 5 249105 would be determined by the definition of beneficial owner in paragraph a. Each one is used to store different information about the interests of owners in a business. Case 15-8 Classification of Stockholders Equity The total owners equity is usually under a number of subcap- tions on the corporations balance sheet. The owners equity is simply the owners share of the assets of a business. And certain instruments that are equity under IFRS could be classified outside equity under US GAAP. Different kinds of equity share capital are authorized issued subscribed paid up rights bonus sweat equity etc.