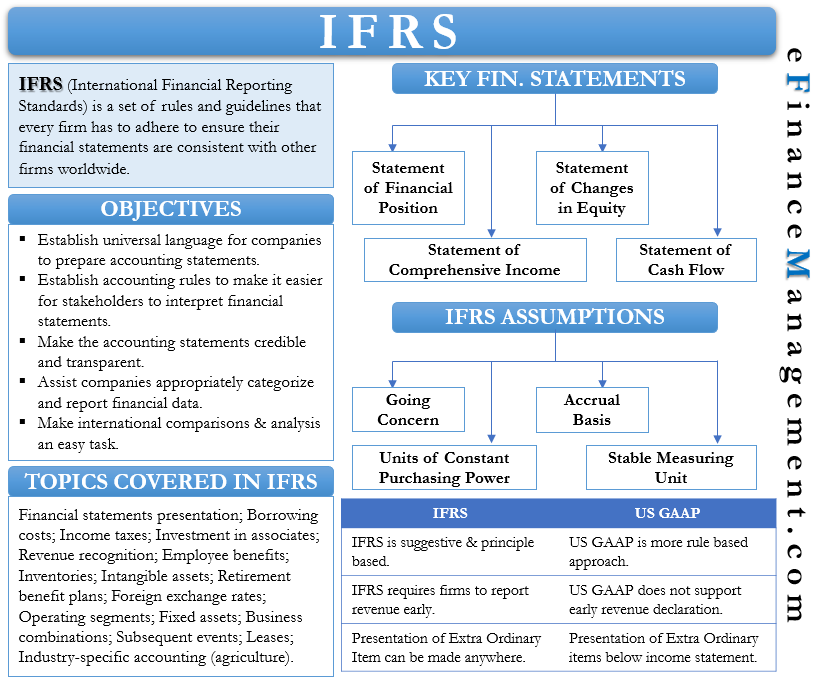

A two statement approach a statement of income and a statement of comprehensive income. Items currently classified as extraordinary are only a subset of the items of income and expense that may warrant disclosure to assist users in predicting an entitys future performance. Extraordinary Items refers to those events which are considered to be unusual by the company as they are infrequent in nature and the gains or losses arising out of these items are disclosed separately in the financial statement of the company during the period in which such item came into the existence. Extraordinary items are defined as being both infrequent and unusual and are rare in practice. An item is unusual if both of the following criteria are met. It possesses a high degree of abnormality. IAS 187 Certain items must be disclosed separately either in the statement of comprehensive income or in the notes if material including. Eliminating the category of extraordinary items eliminates the need for arbitrary segregation of the effects of related external events-some recurring and others not-on the profit or loss of an entity for a. In IFRS extraordinary items are not segregated and are included in the income statement. However the presentation disclosure or characterization of an item as extraordinary is prohibited.

IFRS uses a revaluation model for valuation of fixed assets. Extraordinary items are defined as being both infrequent and unusual and are rare in practice. Extraordinary Items refers to those events which are considered to be unusual by the company as they are infrequent in nature and the gains or losses arising out of these items are disclosed separately in the financial statement of the company during the period in which such item came into the existence. Neither IFRS nor US GAAP allow classification of any item as an extraordinary item in the income statement. Valuation of Fixed Assets. Previously US GAAP allowed classification of certain items as extraordinary items. That standard defined extraordinary items as income or expenses that arise from events or transactions that are clearly distinct from the ordinary activities of the enterprise and therefore are not expected to recur frequently or regularly. Entities may utilize one of three formats in their presentation of comprehensive income. Eliminating the category of extraordinary items eliminates the need for arbitrary segregation of the effects of related external events-some recurring and others not-on the profit or loss of an entity for a. We believe it is possible to characterize items as unusual or exceptional under certain conditions.

However the presentation disclosure or characterization of an item as extraordinary is prohibited. Neither IFRS nor US GAAP allow classification of any item as an extraordinary item in the income statement. We believe it is possible to characterize items as unusual or exceptional under certain conditions. Under IFRS companies are not required to report financial results using a highly detailed set of reporting templates. IAS 187 Certain items must be disclosed separately either in the statement of comprehensive income or in the notes if material including. While the use of templates would offer a high degree of uniformity across companies such use can result in companies reporting a large volume of. In GAAP the extraordinary items are segregated and are shown below net income in the income statement. IFRS uses a revaluation model for valuation of fixed assets. Unusual or exceptional items IFRS does not describe events or items of income or expense as unusual or exceptional. Items currently classified as extraordinary are only a subset of the items of income and expense that may warrant disclosure to assist users in predicting an entitys future performance.

Additional line items may be needed to fairly present the entitys results of operations. The International Financial Reporting Standards IFRS does not recognize extraordinary items only nonrecurring items. A single primary statement of income and comprehensive income. It possesses a high degree of abnormality. Extraordinary Items refers to those events which are considered to be unusual by the company as they are infrequent in nature and the gains or losses arising out of these items are disclosed separately in the financial statement of the company during the period in which such item came into the existence. In IFRS extraordinary items are not segregated and are included in the income statement. Items currently classified as extraordinary are only a subset of the items of income and expense that may warrant disclosure to assist users in predicting an entitys future performance. Neither IFRS nor US GAAP allow classification of any item as an extraordinary item in the income statement. An extraordinary item in accounting is an event or transaction that is considered abnormal not related to ordinary company activities and unlikely to recur in the foreseeable future. Rather all results are disclosed as revenues finance costs post-tax gains or losses or results from associates and joint ventures.

The formal use of extraordinary items has been eliminated under Generally Accepted Accounting Principles so the following discussion should be considered historical in nature. Extraordinary Items refers to those events which are considered to be unusual by the company as they are infrequent in nature and the gains or losses arising out of these items are disclosed separately in the financial statement of the company during the period in which such item came into the existence. IAS 185 Items cannot be presented as extraordinary items in the financial statements or in the notes. The International Financial Reporting Standards IFRS does not recognize extraordinary items only nonrecurring items. Valuation of Fixed Assets. So far International Accounting Standards IASs and International Financial Reporting Standards IFRSs have not defined such terminologies. Eliminating the category of extraordinary items eliminates the need for arbitrary segregation of the effects of related external events-some recurring and others not-on the profit or loss of an entity for a. Items currently classified as extraordinary are only a subset of the items of income and expense that may warrant disclosure to assist users in predicting an entitys future performance. An item is unusual if both of the following criteria are met. A two statement approach a statement of income and a statement of comprehensive income.