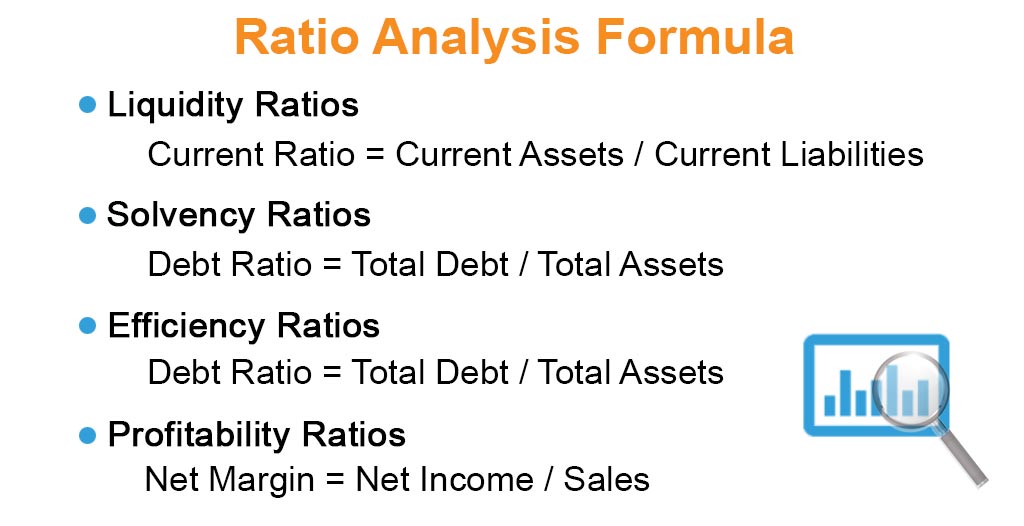

Receivables turnover ratio Net credit sales Average accounts receivable. CRISIL does not adopt an arithmetic approach in using these ratios while assessing financial risk. Financial Statement Analysis - Liquidity Ratios In analyzing Financial Statements for the purpose of granting credit ratios can be broadly classified into three categories. The price-to-earnings ratio aka PE ratio is perhaps the most. This is determined by the monthly recurring debts of a company divided by the gross monthly income. The credit analysis is not only financial analysis. The credit analyst compiles this information and synthesize to get a snapshot of risks weaknesses and reinforcing elements strengths of the business opportunity. Ratios like account receivables turnover Account Receivables Turnover Accounts Receivable turnover also known as debtors turnover estimates how many times a business collects the average accounts receivable per year and is used to evaluate the companys effectiveness in providing a credit facility to its customers and timely collection. These ratios are used to arrive at the cash generation capacity of the company. Below we discuss the mechanics and intuition of some of the most common credit analysis ratios across 4 categories.

Ratios like account receivables turnover Account Receivables Turnover Accounts Receivable turnover also known as debtors turnover estimates how many times a business collects the average accounts receivable per year and is used to evaluate the companys effectiveness in providing a credit facility to its customers and timely collection. The credit analysis is not only financial analysis. Liquidity ratios These ratios deal with the ability of the company to repay its creditors expenses etc. We will discuss few ratios which are predominantly used by credit rating analyst or credit rating agencies to gauge solvency and cash flow related aspects of a businesscompany. Financial ratios are a means of evaluating a companys performance or health using its financial statements. Ratio analysis can be defined as the process of ascertaining the financial ratios that are used for indicating the ongoing financial performance of a company using few types of ratios such as liquidity profitability activity debt market solvency efficiency and coverage ratios and few examples of such ratios are return on equity current ratio quick ratio dividend payout ratio debt. The relative importance of the ratios may vary on a case-specific basis. A detailed discussion on each of the eight parameters is presented below. Important Financial Ratios for Credit Analysis Credit analysis covers the area of analyzing the character of the borrowers capacity to use the loan amount condition of capital objectives of taking a loan planning for uses probable repayment schedule so on. This is determined by the monthly recurring debts of a company divided by the gross monthly income.

The accounts receivable turnover ratio measures how many times a company can turn receivables into cash over a given period. We will discuss few ratios which are predominantly used by credit rating analyst or credit rating agencies to gauge solvency and cash flow related aspects of a businesscompany. Ratios used in Credit Analysis. Financial Statement Analysis - Liquidity Ratios In analyzing Financial Statements for the purpose of granting credit ratios can be broadly classified into three categories. Since debt is in the denominator here a higher ratio means a greater ability to pay debts. Instead CRISIL makes a subjective assessment of the importance of the ratios for each credit. A higher ratio implies more leverage and thus higher credit risk. Credit rating agencies often use this leverage ratio. Ratios like account receivables turnover Account Receivables Turnover Accounts Receivable turnover also known as debtors turnover estimates how many times a business collects the average accounts receivable per year and is used to evaluate the companys effectiveness in providing a credit facility to its customers and timely collection. It goes well beyond it takes into account the entire business environment to determine the risk for the seller to extend credit to the buyer.

Analysts consider various ratios and financial instruments to arrive at the true picture of the company. Ratios used in Credit Analysis. A higher ratio implies more leverage and thus higher credit risk. We will discuss few ratios which are predominantly used by credit rating analyst or credit rating agencies to gauge solvency and cash flow related aspects of a businesscompany. Equity Analysis Valuation Ratios. Individuals with a debt-to-income ratio below 35 are considered as acceptable credit risks. The DSCR is a measure of the level of cash flow available to pay current. There are several approaches to credit analysis that vary and depend on the purpose of the analysis and the context within which the analysis is being done. Below we discuss the mechanics and intuition of some of the most common credit analysis ratios across 4 categories. Credit Analysis Example An example of a financial ratio used in credit analysis is the debt service coverage ratio DSCR.

A higher ratio implies more leverage and thus higher credit risk. Liquidity ratios These ratios deal with the ability of the company to repay its creditors expenses etc. This is determined by the monthly recurring debts of a company divided by the gross monthly income. The DSCR is a measure of the level of cash flow available to pay current. Inventory turnover ratio Cost of goods sold Average inventory. Liquidity refers to the ability of a company to pay. Ratios used in Credit Analysis. The relative importance of the ratios may vary on a case-specific basis. A higher ratio implies more leverage and thus higher credit risk. Important Financial Ratios for Credit Analysis Credit analysis covers the area of analyzing the character of the borrowers capacity to use the loan amount condition of capital objectives of taking a loan planning for uses probable repayment schedule so on.