First Class Royalty Expense On Income Statement Where Is Net Sales

Complete Guide To Income Statements Examples And Templates

First the royalty expense account would be debited for the full royalty amount 7000. A royalty to produce a product would go into COGs. Estates and trusts do not use Form 4835 or Schedule F Form 1040 for this purpose. The following information was taken from the 2004 financial statement of pharmecutical giant Merck and CO. Although indirect costs are not applied to specific cost objects you can allocate costs to determine how much you are spending on expenses compared to your sales. Thus he can count on income only after sales exceed 200000 because he already received an advance royalty payment for this sales amount in the beginning. Retained earnings January 1 2004 341420 Materials and production expense 49598 Marketing and administrative expense 73463 Dividends 33291. A franchisee pays the same amount in regular royalty fees regardless of how the franchise is performing. 46 Royalties and income taxes 85 461 Petroleum taxes royalty and excise 85 462 Petroleum taxes based on profits 85 463 Taxes paid in cash or in kind 89 464 Deferred tax and acquisitions of participating interests in jointly controlled assets 89 465 Discounting of petroleum taxes 90. Because the production-based royalties are not income taxes the royalty payments should not be presented as an income tax expense in the statement of comprehensive income.

It is the cost that the buyer bears to use the goodsservices provided by the owner.

This helps in getting the tax benefit over the asset. The return on investment of these costs is what defines a companys health. Because the production-based royalties are not income taxes the royalty payments should not be presented as an income tax expense in the statement of comprehensive income. For brokers commissions and royalties and other payments to organizations selling our product these are always in Selling Expense. For example there are a couple of manufacturing processes in which we pay royalties for a process so we put this in COGS. For an estate or trust only farm rental income and expenses based on crops or livestock produced by the tenant.

Different business models and industries require different operating expenses. The return on investment of these costs is what defines a companys health. Because the production-based royalties are not income taxes the royalty payments should not be presented as an income tax expense in the statement of comprehensive income. The prepaid royalty account now only totals 3000 10000 original minus 7000. 12 Alliances and royalty expenses Income statement geography is an open topic Current accounting and reporting rules. Retained earnings January 1 2004 341420 Materials and production expense 49598 Marketing and administrative expense 73463 Dividends 33291. All dollar amounts are in millions. The following information was taken from the 2004 financial statement of pharmecutical giant Merck and CO. The total royalty payment 7 percent of 100000 or 7000 would be debited to the royalty expense account and credited to the prepaid royalties account. For brokers commissions and royalties and other payments to organizations selling our product these are always in Selling Expense.

It is the cost that the buyer bears to use the goodsservices provided by the owner. A royalty to produce a product would go into COGs. Find out the revenue expenses and profit or loss over the last fiscal year. For brokers commissions and royalties and other payments to organizations selling our product these are always in Selling Expense. The return on investment of these costs is what defines a companys health. Operating expenses on an income statement are costs that arise in the normal course of business. It is a one time expense and can be put under the asset category. First the royalty expense account would be debited for the full royalty amount 7000. Royalty is a purchasing expense. Although indirect costs are not applied to specific cost objects you can allocate costs to determine how much you are spending on expenses compared to your sales.

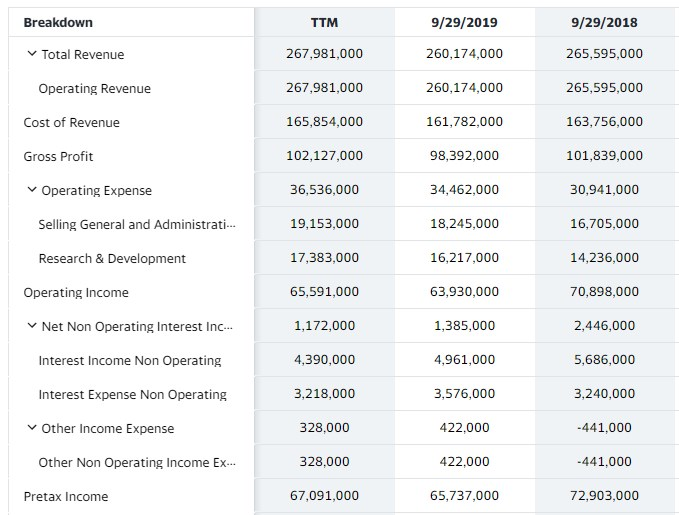

It is a one time expense and can be put under the asset category. Retained earnings January 1 2004 341420 Materials and production expense 49598 Marketing and administrative expense 73463 Dividends 33291. Thus he can count on income only after sales exceed 200000 because he already received an advance royalty payment for this sales amount in the beginning. If you pay more than 10 in royalties in a year you must give the payee a 1099-MISC form to show the total of your payments for the year. For an estate or trust only farm rental income and expenses based on crops or livestock produced by the tenant. Get the detailed quarterlyannual income statement for Royalty Pharma plc RPRX. For example there are a couple of manufacturing processes in which we pay royalties for a process so we put this in COGS. The Committee considered that in the light of its analysis of the existing requirements of IAS 1 and IAS 12 an interpretation was not necessary and consequently decided not to add this issue to its agenda. Estates and trusts do not use Form 4835 or Schedule F Form 1040 for this purpose. 12 Alliances and royalty expenses Income statement geography is an open topic Current accounting and reporting rules.

Estates and trusts do not use Form 4835 or Schedule F Form 1040 for this purpose. Because the production-based royalties are not income taxes the royalty payments should not be presented as an income tax expense in the statement of comprehensive income. Includes royalty expenses on royalty income notably MabThera royalties paid by Genentech to Biogen Idec on the royalties paid by Roche to Genentech as well as back royalties and other true-ups. If your direct costs are also high you wont be turning much of a profit. Just so how are royalty payments calculated. Assuming net income remained the same for the next period a different set of entries would be made. Income Statement Classification of Royalty Expense Businesses create income statements for each accounting cycle typically on a yearly basis. A royalty to produce a product would go into COGs. Retained earnings January 1 2004 341420 Materials and production expense 49598 Marketing and administrative expense 73463 Dividends 33291. Get the detailed quarterlyannual income statement for Royalty Pharma plc RPRX.

For brokers commissions and royalties and other payments to organizations selling our product these are always in Selling Expense. Because the production-based royalties are not income taxes the royalty payments should not be presented as an income tax expense in the statement of comprehensive income. 46 Royalties and income taxes 85 461 Petroleum taxes royalty and excise 85 462 Petroleum taxes based on profits 85 463 Taxes paid in cash or in kind 89 464 Deferred tax and acquisitions of participating interests in jointly controlled assets 89 465 Discounting of petroleum taxes 90. A royalty to produce a product would go into COGs. Thus he can count on income only after sales exceed 200000 because he already received an advance royalty payment for this sales amount in the beginning. Royalty is a purchasing expense. First the royalty expense account would be debited for the full royalty amount 7000. This helps in getting the tax benefit over the asset. Get the detailed quarterlyannual income statement for Royalty Pharma plc RPRX. The total royalty payment 7 percent of 100000 or 7000 would be debited to the royalty expense account and credited to the prepaid royalties account.