Out Of This World Unrealised Profit In Manufacturing Account Jana Bank Balance Sheet

Manufacturing Account

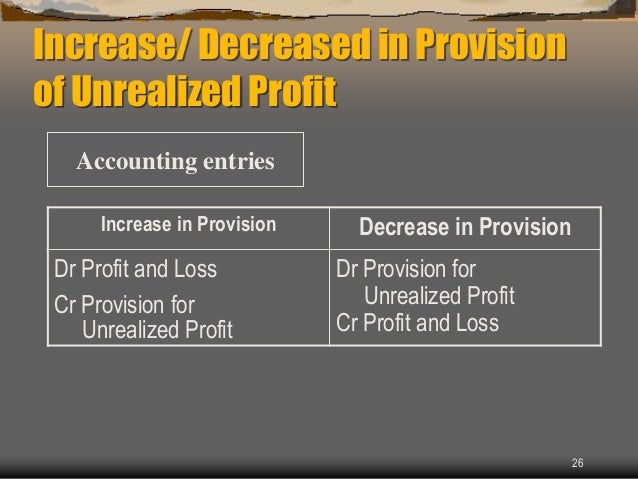

Provision for unrealized profit Mark up 100 Mark up Stock at transfer price x 22. The unrealised profit ie. Inventory should be valued at the lower. If anyone has a document which explains the entire process of configuring and treatment of Unrealised. Unrealised profit is basically internally generated profit that hasnt been passed on to external customers yet. Here is the video about trading and Manufacturing Account Simple explanation with solved problem. This provision for unrealised profit on unsold stock should be treated in the same way as any other provision. So Unrealised profit is profit made between group companies and REMAINS IN STOCK. This means that the change in the provision should appear in the profit and loss account as a debit if it is increased or as a credit if it is decreased which means this. Cost of production Finished good at cost At the beginning of the year At the end of the year Sales 10000 6000 2000 27000 The goods are transferred from factory to sales department at 10 mark-up.

Goods are transferred from the manufacturing Account to the income statement at a factory cost of production plus a markup of 20.

Link for PlayList Financial accounting tutorial collections. Can anyone help me to understand on How BPC 100 NW can support this function. If inventory of finished goods is at cost. The unrealised profit ie. The reason why it is important from an accounting perspective is because it can. The trading account shows Gross Profit.

Goods are transferred from the manufacturing Account to the income statement at a factory cost of production plus a markup of 20. Goods at market value rather than at cost. The use and preparation of the trading and profit and loss accounts are more fully discussed in our trading profit and loss account post. 33 rows Why do you have to adjust for unrealised profit. For the purpose of Legal consolidationI have to remove Unrealised profit on Inventory held in affiliated books at BPC 100 NW. Whereas the Manufacturing Account depicts the cost of goods sold and also includes direct expenses. The reason why it is important from an accounting perspective is because it can. Adjustment for unrealised profit in the transfer of non-current assets Occasionally a non-current asset is transferred within the group say from a parent to a subsidiary. Here is the video about trading and Manufacturing Account Simple explanation with solved problem. If anyone has a document which explains the entire process of configuring and treatment of Unrealised.

Unrealized Profit occurs where it is the policy of the firm to value stocks of finished. Unrealised profits are essentially the profit element one company in a group for example subsidiary makes when it sells inventory to another company in the same group for example to the parent company. The unrealised profit ie. Published on Sep 18 2015. Profit and Loss Accounts b Provision for unrealised profit on stock is calculated. The manufacturing account helps to better the cost-effectiveness of manufacturing activities. Link for PlayList Financial accounting tutorial collections. So Unrealised profit is profit made between group companies and REMAINS IN STOCK. If anyone has a document which explains the entire process of configuring and treatment of Unrealised. An unrealized gain is a potential profit that exists on paper resulting from an investment.

If the stock leaves the group it has become realised. The use and preparation of the trading and profit and loss accounts are more fully discussed in our trading profit and loss account post. - Overstate inventory values. 21 Provision of Unrealized Profit Be made on the closing stock valued at production cost plus a percentage of factory profit. Goods at market value rather than at cost. An unrealized gain is a potential profit that exists on paper resulting from an investment. In the example attached it is the 20 mark up detailed. For this purpose a provision for unrealised profit is set up and maintained. Published on Sep 18 2015. This provision for unrealised profit on unsold stock should be treated in the same way as any other provision.

Consolidated profits are therefore realised profits as they result from dealing with entities external to the group. 21 Provision of Unrealized Profit Be made on the closing stock valued at production cost plus a percentage of factory profit. Profits made by transacting within the group are unrealised. For this purpose a provision for unrealised profit is set up and maintained. Provision for unrealised profit on stock is calculated. Profit and Loss Accounts b Provision for unrealised profit on stock is calculated. In the example attached it is the 20 mark up detailed. A sample Income statement showing this is shown below. In the balance sheet the total PUP is deducted from the inventory of. The factory profit included in the value of closing finished goods inventory is known as.

23 A company manufactures and sells it own products. This provision for unrealised profit on unsold stock should be treated in the same way as any other provision. An unrealized gain is a potential profit that exists on paper resulting from an investment. The manufacturing account helps to better the cost-effectiveness of manufacturing activities. - Overstate inventory values. Inventory should be valued at the lower. Unrealized Profit occurs where it is the policy of the firm to value stocks of finished. Unrealised profits are essentially the profit element one company in a group for example subsidiary makes when it sells inventory to another company in the same group for example to the parent company. Profit and Loss Accounts b Provision for unrealised profit on stock is calculated. The trading profit and loss account of a manufacturing business is similar in format to that of a merchandising business except that purchases is replaced by the manufacturing cost of goods completed.